The new fiscal year begins on 6 April, bringing several important tax changes that could affect your financial plan.

In some cases, tax increases or frozen thresholds could mean that you pay more in the future. Fortunately, if you’re aware of what is changing, you can explore ways to limit the effects on your finances, and we can support you here.

Ultimately, this means you can retain more of your wealth to contribute to important goals for the future.

Here are three tax changes coming into effect on 6 April 2026 and how we can help you respond.

1. Dividend Tax rates are increasing

If you own shares in a company, you may receive a portion of the business’s profits in the form of dividends.

For investors, this might provide a valuable source of income, or you could reinvest dividends to grow your portfolio faster.

If you’re a business owner, dividends might be an important part of your strategy for extracting wealth from the company in a tax-efficient manner.

In both cases, it’s important to consider the tax on your dividends, and you could pay more after 6 April because of upcoming changes.

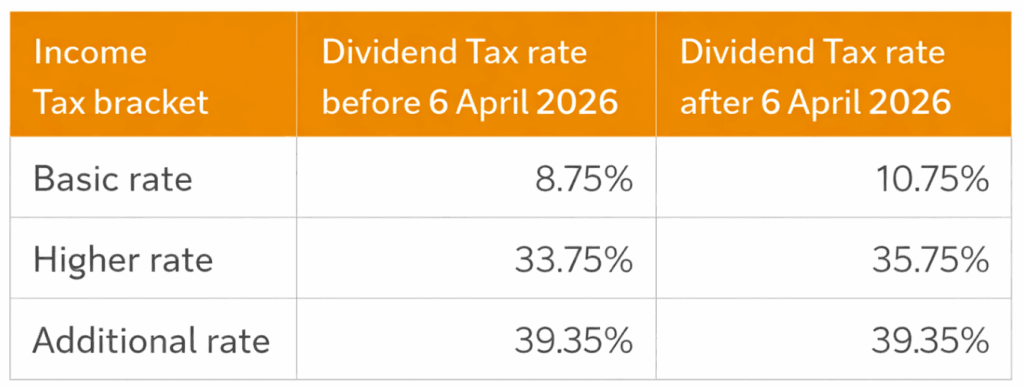

The first £500 of dividend income is tax free – this is your Dividend Allowance. Any dividends that exceed this threshold are subject to Dividend Tax, and the rate you pay depends on your marginal rate of Income Tax.

Crucially, in her 2025 Budget, the chancellor announced that the basic and higher rates of Dividend Tax would increase by two percentage points. The additional rate will remain the same.

The following table shows how much Dividend Tax you could pay before and after 6 April.

Once the change comes into effect, you could pay more Dividend Tax.

For instance, if you earned £5,000 in dividends from shares held outside an ISA, you would pay tax on the remaining £4,500 once you apply your Dividend Allowance.

As a higher-rate taxpayer, before 6 April, you would pay £1,518.75.

After the tax rise comes into effect, you would pay £1,608.75.

If you’re regularly earning income from dividends, this extra tax could add up to a significant amount over time.

Making use of tax wrappers could shield you from Dividend Tax

Although your dividends may be subject to tax, there are useful tax wrappers you can use to help you reduce your bill.

When you invest through a Stocks and Shares ISA, there is no Dividend Tax to pay. You also won’t pay Capital Gains Tax (CGT) when selling shares for a profit.

You can contribute up to £20,000 across all your ISAs each year, so using this full allowance before investing in a General Investment Account could help you improve tax-efficiency.

If you’ve already used your ISA allowance for the year and want to continue investing, you might also consider increasing your pension contributions because shares held in your pension don’t attract Dividend Tax or CGT either.

However, bear in mind that you won’t be able to access these funds until you reach the normal minimum pension age of 55, rising to 57 from 2028.

We can help you make effective use of all the tax wrappers at your disposal.

If you’re a business owner, you may need to reconsider how you draw income from your business. That said, dividends will still be taxed at a lower rate than your salary, even after the increase.

2. Inheritance Tax exemptions for business and agricultural assets are changing

The government has announced several upcoming changes to Inheritance Tax (IHT) rules in recent years. Changes to Business Relief (BR) and Agricultural Relief (AR) are among the most controversial, with the government adjusting the plans in response to criticism.

However, the new rules are now confirmed and will take effect on 6 April 2026.

If you’re a business owner or own certain types of investments, these legislative changes could mean your family pays more IHT on your estate in the future.

Currently, you can benefit from 100% AR on agricultural property, meaning these assets don’t count towards the value of your estate when calculating the IHT owed.

Similarly, you receive 100% BR on:

- A business or interest in a business

- Shares in an unlisted company.

You may also qualify for 50% relief on:

- Shares controlling more than 50% of the voting rights in a listed company

- Land, buildings, or machinery owned by a business that you control or are a partner in.

These reliefs mean that, if you’re a business owner, you can pass on a significant portion of your estate tax-efficiently. Unfortunately, the amount of IHT relief you can benefit from is changing on 6 April 2026.

After this date, there will be a total cap on the amount of combined BR and AR you can benefit from. This was initially set at £1 million before the government revised it to £2.5 million.

This is an individual cap, so a couple can benefit from 100% relief on up to £5 million worth of qualifying assets.

Any assets that exceed the cap will qualify for 50% IHT relief.

Additionally, the rate of BR on shares in unlisted companies will be reduced to 50% in all cases. However, these assets will not count towards the £2.5 million cap.

You may need to revisit your estate plan after the changes

If you’re a business owner or own certain shares that qualify for AR or BR, these changes could make it far more difficult to pass wealth to your loved ones tax-efficiently.

As such, you may need to revisit your estate plan and explore IHT-planning strategies. We can help you here by:

- Making sure you use all the available IHT allowances and exemptions

- Creating a gifting strategy to pass wealth to your loved ones while alive

- Placing a life insurance policy in a trust to help your beneficiaries manage a large IHT bill.

With our support, you can adapt to the changing IHT landscape after changes to BR and AR.

3. Frozen Income Tax thresholds could mean you face a higher bill

During the 2025 Budget, the chancellor confirmed an extension of the freeze on Income Tax thresholds until April 2031. While this wasn’t a specific change, the decision to continue the freeze could have a marked effect on the amount you pay.

To understand why, it’s important to consider how your Income Tax is calculated.

As of 2025/26, the first £12,570 you earn is tax free.

You will then pay:

- 20% on earnings between £12,571 and £50,270

- 40% on earnings between £50,271 and £125,140

- 45% on earnings over £125,140.

Prior to April 2021, when the government first introduced the freeze, these thresholds would usually increase each year. This meant that, as the cost of living rose and wages went up, the Income Tax thresholds rose at a similar pace.

Now, the thresholds are frozen, but wages continue to rise. According to the Office for National Statistics (ONS), average weekly total earnings in April 2021 were £576. By December 2025, that had risen to £735.

This means that more of your earnings are pulled into the taxable range, and you could be more likely to move into a higher tax bracket.

After the Budget, the Independent reported that the freeze was expected to create:

- 780,000 more basic-rate taxpayers

- 920,000 more higher-rate taxpayers

- 4,000 more additional-rate taxpayers.

As the freeze will likely be in place until at least April 2031, it’s important to consider how this increased tax burden could affect your disposable income and ability to save for the future.

Increasing pension contributions could help you reduce Income Tax

Employing strategies to reduce Income Tax could mean you retain more of your wealth and limit the impact of frozen thresholds.

Contributing to your pension is one way to achieve this, as you benefit from Income Tax relief on your contributions. By paying more into your pensions, you could reduce your taxable income and, in some cases, avoid moving into a higher tax bracket.

However, as discussed earlier, there are limits on when you can access wealth in your pensions, so you will need to consider whether increasing your contributions is suitable for you.

We can discuss the most suitable ways to manage your Income Tax liability.

Get in touch

If you are concerned about how these upcoming changes could affect you, we can help.

Please get in touch or email us at advice@mlifa.co.uk for more information.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate estate planning or tax planning.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.