From 6 April 2026, a range of new tax rules came into effect.

Among them was an increase in Dividend Tax, which will see those paying the basic and higher rates pay two percentage points more tax on their dividend income.

This is just the latest in a range of Dividend Tax changes over the last decade.

Read more: Three tax changes taking effect from 6 April 2026 and what you can do to mitigate them

Over the last decade, the government has reduced the tax-free Dividend Allowance and increased rates

You are usually liable to pay Dividend Tax on the income you make from holding shares in a company. The rate of tax you pay is based on your Income Tax band.

The modern system for Dividend Tax came into effect in the 2016/17 financial year, replacing the notional 10% tax credit system, which previously allowed basic-rate taxpayers 100% relief.

Under the new system, the Dividend Allowance was introduced, providing Dividend Tax relief on income up to £5,000. Dividend Tax rates became fixed at:

- 7.5% for basic-rate taxpayers

- 32.5% for higher-rate taxpayers

- 38.1% for additional-rate taxpayers.

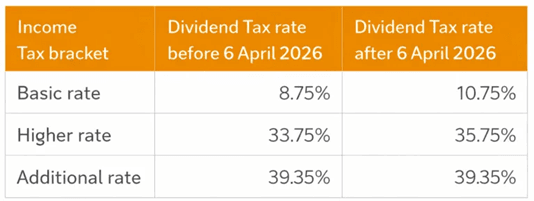

By 2024, the Dividend Allowance had been reduced to £500, and Dividend Tax rates had been increased to:

- 8.75% for basic-rate taxpayers

- 33.75% for higher-rate taxpayers

- 39.35% for additional-rate taxpayers.

These changes impacted everyone who earned income from dividends, provided the earnings exceed the Dividend Allowance.

For example, a higher-rate taxpayer receiving £10,000 in dividend income in 2016 would have been liable to pay £1,625. In 2024, this would have increased to £3,206.

These gradual restrictions on dividend income have made it more difficult for UK savers to accumulate wealth from their investments.

New Dividend Tax hikes came into effect on 6 April 2026

As of 6 April 2026, Dividend Tax has increased by a further two percentage points for basic- and higher-rate taxpayers.

These changes were first announced in the 2025 Autumn Budget, along with the introduction of separate tax rates for property income and an increase to the tax rate on savings income. According to the House of Commons Library, these measures are forecast to raise around £2.3 billion a year between 2028/29 and 2030/31.

A higher-rate taxpayer earning £10,000 of dividend income annually (outside of ISAs) would now be liable for £3,396 in Dividend Tax – £190 more than the previous tax year.

The more you rely on dividend income, the more you might be affected. For example, if your dividend income was £20,000, as a higher-rate taxpayer, your Dividend Tax liability would increase by £390 for the 2026/27 tax year compared to the previous tax year.

Only additional-rate taxpayers are unaffected by the Dividend Tax rise.

Three ways you can mitigate a higher Dividend Tax bill

There are several strategies you can implement to reduce your overall Dividend Tax liability.

- Maximise your ISA allowance each year

Wealth in an ISA is free from Income Tax, Capital Gains Tax (CGT), and, crucially, Dividend Tax.

This relief exists up to the annual subscription limit of £20,000, which is shared across all adult ISA types, including:

- Cash ISAs

- Stocks and Shares ISAs

- Innovative Finance ISAs

- Lifetime ISAs (LISAs)

Note that the Cash ISA annual subscription amount is reducing to £12,000 for under-65s from April 2027. However, the subscription limit remains at £20,000 for other ISA types.

Making the most of your ISA contributions each year means you could limit the Dividend Tax you pay.

- Increase your pension contributions

Like ISAs, pensions benefit from generous tax relief.

Tax relief on pension contributions is available up to your Annual Allowance, which is the lower of £60,000 or 100% of your earnings.

This option is particularly useful for those using dividend income to accumulate long-term wealth for retirement.

However, if you use dividend income for more short-term needs, ISAs offer much more flexibility.

- Plan with your partner

You can organise your finances to take advantage of both your and your partner’s tax-relief opportunities.

For example, dividing your invested wealth between you and your significant other means you can take advantage of a combined Dividend Allowance and ISA allowance.

You can also strategically reduce your overall Dividend Tax liability by transferring assets to your partner if they are in a lower tax band.

For example, if your partner pays the basic rate of tax while you are in the higher tax bracket, transferring invested assets producing £10,000 in dividend income could reduce your tax liability by £2,375.

Get in touch

If you’re concerned about a higher Dividend Tax bill this year, we can help you determine whether you’re affected and what strategies can best help you mitigate an increased liability.

Please get in touch or email us at advice@mlifa.co.uk for more information.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate tax planning.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.